Adjusting Entries

Why adjusting entries are needed

In order for a company's financial statements to be complete and to reflect the accrual method of accounting, adjusting entries must be processed before the financial statements are issued. Here are three situations that describe why adjusting entries are needed:

Situation 1

Not all of a company's financial transactions that pertain to an accounting period will have been processed by the accounting software as of the end of the accounting period. For example, the bill for the electricity used during December might not arrive until January 10. (The reason for the 10-day lag is that the electric utility reads the meters on January 1 in order to compute the electricity actually used in December. Next the utility has to prepare the bill and mail it to the company.)

Situation 2

Sometimes a bill is processed during the accounting period, but the amount represents the expense for one or more future accounting periods. For example, the bill for the insurance on the company's vehicles might be $6,000 and covers the six-month period of January 1 through June 30. If the company is required to pay the $6,000 in advance at the end of December, the expense needs to be deferred so that $1,000 will appear on each of the monthly income statements for January through June.

Situation 3

Something similar to Situation 2 occurs when a company purchases equipment to be used in the business. Let's assume that the equipment is acquired, paid for, and put into service on May 1. However, the equipment is expected to be used for ten years. If the cost of the equipment is $120,000 and will have no salvage value, then each month's income statement needs to report $1,000 for 120 months in order to report depreciation expense under the straight-line method.

These three situations illustrate why adjusting entries need to be entered in the accounting software in order to have accurate financial statements. Unfortunately the accounting software cannot compute the amounts needed for the adjusting entries. A bookkeeper or accountant must review the situations and then determine the amounts needed in each adjusting entry.

Steps for Recording Adjusting Entries

Some of the necessary steps for recording adjusting entries are

- You must identify the two or more accounts involved

- One of the accounts will be a balance sheet account

- The other account will be an income statement account

- You must calculate the amounts for the adjusting entries

- You will enter both of the accounts and the adjustment in the general journal

- You must designate which account will be debited and which will be credited.

Types of Adjusting Entries

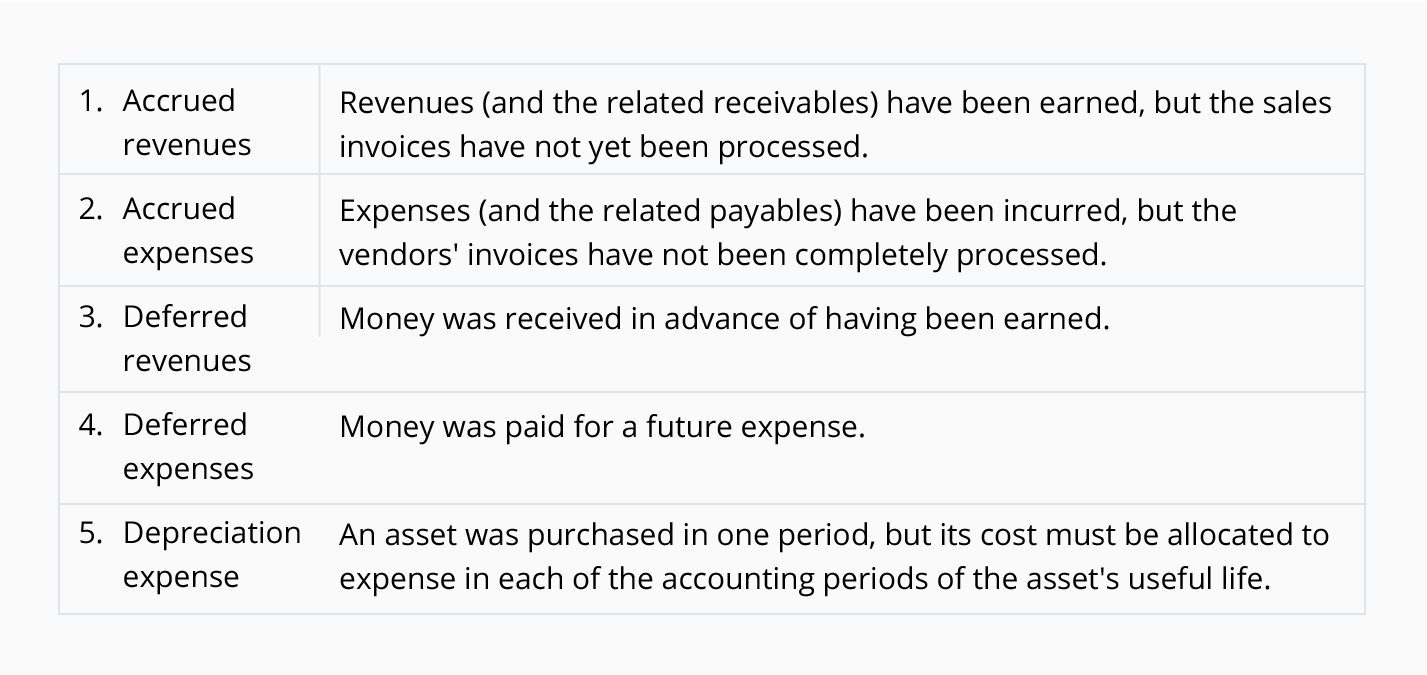

We will sort the adjusting entries into five categories.

1. Accrued revenues

Under the accrual method of accounting, a business is to report all of the revenues (and related receivables) that it has earned during an accounting period. A business may have earned fees from having provided services to clients, but the accounting records do not yet contain the revenues or the receivables. If that is the case, an accrual-type adjusting entry must be made in order for the financial statements to report the revenues and the related receivables.

If a business has earned $5,000 of revenues, but they are not recorded as of the end of the accounting period, the accrual-type adjusting entry will be as follows:

2. Accrued expenses

Under the accrual method of accounting, the financial statements of a business must report all of the expenses (and related payables) that it has incurred during an accounting period. For example, a business needs to report an expense that has occurred even if a supplier's invoice has not yet been received.

To illustrate, let's assume that a company utilized a worker from a temporary personnel agency on December 27. The company expects to receive an invoice on January 2 and remit payment on January 9. Since the expense and the payable occurred in December, the company needs to accrue the expense and liability as of December 31 with the following adjusting entry:

3. Deferred revenues

Under the accrual method of accounting, the amounts received in advance of being earned must be deferred to a liability account until they are earned.

Let's assume that Servco Company receives $4,000 on December 10 for services it will provide at a later date. Prior to issuing its December financial statements, Servco must determine how much of the $4,000 has been earned as of December 31. The reason is that only the amount that has been earned can be included in December's revenues. The amount that is not earned as of December 31 must be reported as a liability on the December 31 balance sheet.

If $3,000 has been earned, the Service Revenues account must include $3,000. The remaining $1,000 that has not been earned will be deferred to the following accounting period. The deferral will be evidenced by a credit of $1,000 in a liability account such as Deferred Revenues or Unearned Revenues.

The adjusting entry for this deferral depends on how the receipt of $4,000 was recorded on December 10. If the receipt of $4,000 was recorded with a credit to Service Revenues (and a debit to Cash), the December 31 adjusting entry will be:

If the entire receipt of $4,000 had been credited to Deferred Revenues on December 10 (along with a debit to Cash), the adjusting entry on December 31 would be:

4. Deferred expenses

Under the accrual method of accounting, any payments for future expenses must be deferred to an asset account until the expenses are used up or have expired.

To illustrate, let's assume that a new company pays $6,000 on December 27 for the insurance on its vehicles for the six-month period beginning January 1. For December 27 through 31, the company should have an asset Prepaid Insurance or Prepaid Expenses of $6,000.

In each of the months January through June, the company must reduce the asset account by recording the following adjusting entry:

5. Depreciation expense

Depreciation is associated with fixed assets (or plant assets) that are used in the business. Examples of fixed assets are buildings, machinery, equipment, vehicles, furniture, and other constructed assets used in a business and having a useful life of more than one year. (However, land is not depreciated.)

Depreciation allocates the asset's cost (minus any expected salvage value) to expense in the accounting periods in which the asset is used. Hence, office equipment with a useful life of 5 years and no salvage value will mean monthly depreciation expense of 1/60 of the equipment's cost. A building with a useful life of 25 years and no salvage value will result in a monthly depreciation expense of 1/300 of the building's cost.

No comments:

Post a Comment