Asset accounts are one of the three major classifications of balance sheet accounts:

- Assets

- Liabilities

- Stockholders' equity (or owner's equity)

The ending balances in the balance sheet accounts will be carried forward to the next accounting year. Hence the balance sheet accounts are called permanent accounts or real accounts.

The asset accounts are usually listed first in the company's chart of accounts and in the general ledger. In the general ledger the asset accounts will normally have debit balances.

The balances in some of the asset accounts will be combined and presented as a single amount when the balance sheet is prepared. For example, if a company has ten checking accounts, the balances will be combined and the total amount will be reported on the balance sheet as the asset Cash.

Assets include the things or resources that a company owns, that were acquired in a transaction, and have a future value that can be measured. Assets also include some costs that are prepaid or deferred and will become expenses as the costs are used up over time.

Here are some examples of asset accounts:

- Cash

- Short-term Investments

- Accounts Receivable

- Allowance for Doubtful Accounts (a contra-asset account)

- Accrued Revenues/Receivables

- Prepaid Expenses

- Inventory

- Supplies

- Long-term Investments

- Land

- Buildings

- Equipment

- Vehicles

- Furniture and Fixtures

- Accumulated Depreciation (a contra-asset account)

Descriptions of asset accounts

The following are brief descriptions of some common asset accounts.

Cash

Cash includes currency, coins, checking account balances, petty cash funds, and customers' checks that have not yet been deposited. A company is likely to have a separate general ledger account for each checking account, petty cash fund, etc. but will combine the amounts and will report the total as Cash (or Cash and Cash Equivalents) on the balance sheet.

Short-term Investments

Short-term or temporary investments may include certificates of deposit, bonds, notes, etc. that will mature in less than one year. It may also include investments in the common or preferred stock of another corporation if the stock can be easily sold on a stock exchange.

Accounts Receivable

Accounts receivable is a right to receive an amount as the result of delivering goods or services on credit. Under the accrual method of accounting, Accounts Receivable is debited at the time of a credit sale. Later, when the customer pays the amount owed, the company will credit Accounts Receivable (and will debit Cash).

Allowance for Doubtful Accounts

The Allowance for Doubtful Accounts is a contra-asset account since its balance is intended to be a credit balance (or a zero balance). When the balance in this account is combined with the balance in Accounts Receivable, the resulting amount is known as the net realizable value of the receivables. The Allowance for Doubtful Accounts is used under the allowance method of reporting bad debts expense.

Accrued Revenues/Receivables

Under the accrual method of accounting, revenues are to be reported when goods or services have been delivered even if a sales invoice has not been generated. This account will report the amounts that a company has a right to receive but the sales invoices have yet to be prepared or entered in Accounts Receivable.

Prepaid Expenses

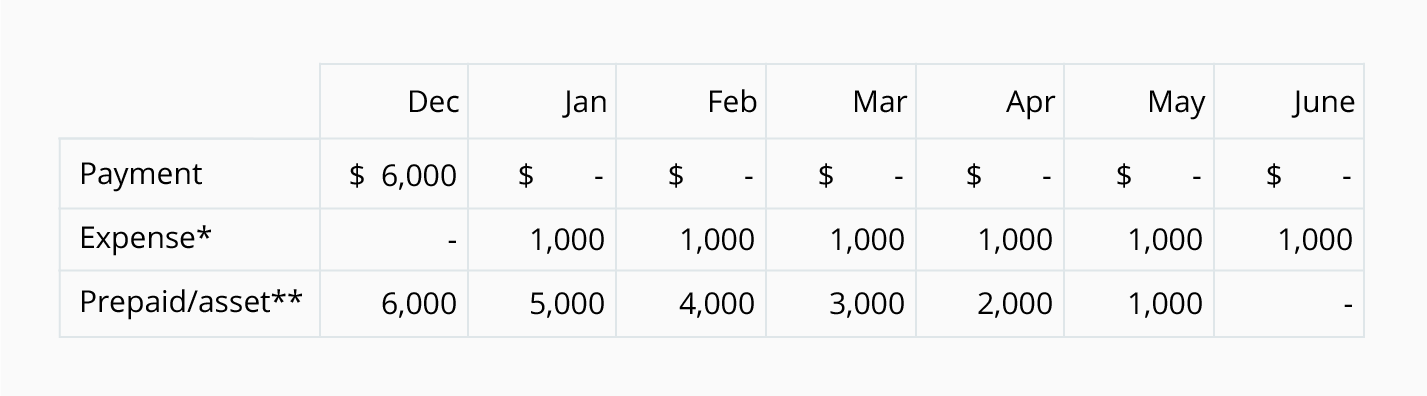

These are future expenses that have already been paid. The amounts appear as assets until the costs have been used up or expire. A common example of a prepaid expense is the payment for vehicle insurance. To illustrate this, let's assume that on December 29, a new company pays $6,000 for the insurance covering its vehicles for the six-month period that will begin on January 1. As of December 31, the entire $6,000 will be a prepaid expense because none of the cost has expired. Since none of the cost expired in December, there is no insurance expense in December. The insurance expense will begin in January at a rate of $1,000 per month. This is depicted in the following chart:

*The expense is the amount that is expiring during the month.

**The prepaid amounts are the unexpired amounts and should be the balance in the asset account Prepaid Expenses or Prepaid Insurance at the end of each of the months.

Inventory

Inventory is the cost of goods that have been purchased or manufactured and have not yet been sold.

Supplies

Supplies could be office supplies, manufacturing supplies, packaging supplies or other supplies that are on hand. The cost of the supplies that remain on hand is reported as an asset.

Long-term Investments

This account or asset category will be reported on the balance sheet immediately following current assets. It may include investments in the common stock, preferred stock, and bonds of another corporation. It also includes real estate being held for sale and also the money that is restricted for a long-term purpose such as a building project or the repurchase of bonds payable. The cash surrender value of a life insurance policy owned by a company is also reported under this asset heading.

Land

This account represents the property portion of the balance sheet heading "Property, plant and equipment." It reports the cost of land used in a business. Since land is assumed to last indefinitely, the cost of land is not depreciated.

Buildings

This account will report the cost of the building used in the business. The cost of buildings will be depreciated over their useful lives.

Equipment

This account reports the cost of the machinery and equipment used in the business. The cost of equipment will be depreciated over the equipment's useful life.

Vehicles

This account reports the cost of trucks, trailers, and automobiles used in the business. The cost of vehicles is to be depreciated over the vehicles' useful lives.

Furniture and Fixtures

This account reports the cost of desks, chairs, shelving, etc. that are used in the business. The cost of furniture and fixtures is to be depreciated over the useful lives.

Accumulated Depreciation

Accumulated Depreciation is known as a contra asset account because it has a credit balance instead of a debit balance that is typical for asset accounts. Whenever Depreciation Expense is debited for the periodic depreciation of the buildings, equipment, vehicles, etc. the account Accumulated Depreciation is credited. The credit balance in Accumulated Depreciation will continue to grow until an asset is sold or scrapped. However, the maximum amount of the credit balance is the cost of the asset(s).

No comments:

Post a Comment