The balance sheet is one of the four main financial statements of a business:

- Balance Sheet

- Income Statement

- Cash Flow Statement

- Statement of Stockholders' Equity

The balance sheet reports a company's assets, liabilities, and stockholders' equity as of a moment in time. (The other three financial statements report amounts for a period of time such as a year, quarter, month, etc.) The balance sheet is also known as the statement of financial position and it reflects the accounting equation:

Assets = Liabilities + Stockholders' Equity.

Bankers will look at the balance sheet to determine the amount of a company's working capital, which is the amount of current assets minus the amount of current liabilities. They will also review the assets and the liabilities and compare these amounts to the amount of stockholders' equity.

When a balance sheet reports at least one additional column of amounts from an earlier balance sheet date, it is referred to as a comparative balance sheet.

Balance Sheet Classifications

Typically, companies issue a classified balance sheet. This means that the amounts are presented according to the following classifications:

Descriptions of the balance sheet classifications

The following are brief descriptions of the classifications usually found on a company's balance sheet.

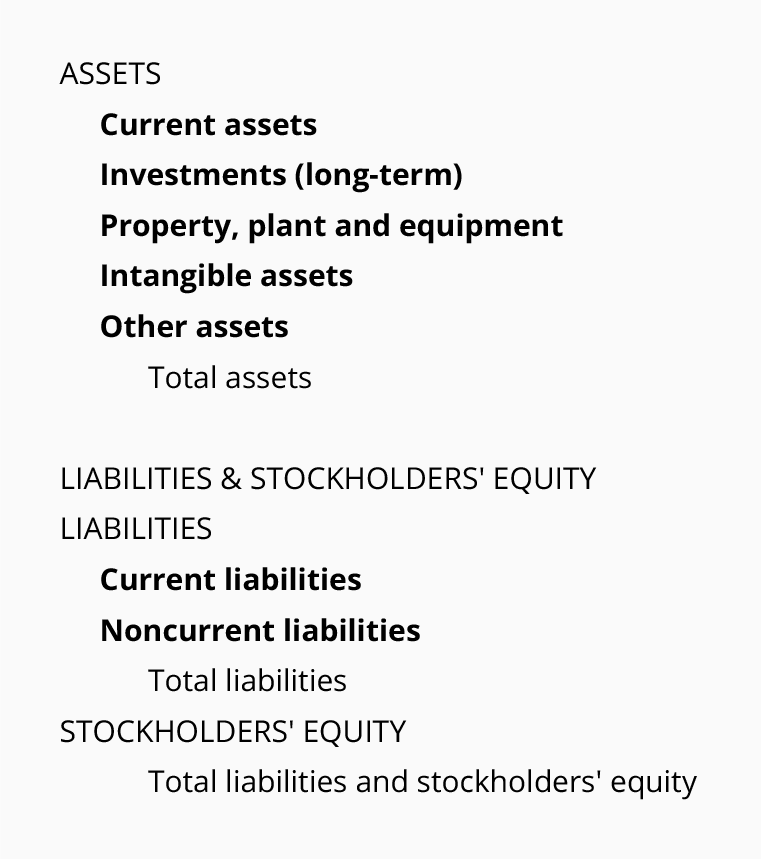

Current assets

Generally, current assets include cash and other assets that are expected to turn to cash within one year of the date of the balance sheet. Examples of current assets are cash and cash equivalents, short-term investments, accounts receivable, inventory and prepaid expenses.

Investments

This classification is the first of the noncurrent or long-term assets. Included are long-term investments in other companies, the cash surrender value of life insurance, bond sinking funds, real estate held for sale, and cash that is restricted for construction of plant and equipment.

Property, plant and equipment

This category of noncurrent assets includes the cost of land, buildings, machinery, equipment, furniture, fixtures, and vehicles used in the operations of a business. Except for land, these assets will be depreciated over their useful lives.

Intangible assets

Intangible assets include goodwill, trademarks, patents, copyrights and other non-physical assets that were acquired at a cost. The amount reported is their cost to acquire minus any amortization or write-down due to impairment. Valuable trademarks and logos that were developed by a company through years of advertising are not reported because they were not purchased from another person or company.

Other assets

This category often includes costs that have been paid but are being expensed over a period greater than one year. Examples include bond issue costs and certain deferred income taxes.

Current liabilities

Current liabilities are obligations of a company that are payable within one year of the date of the balance sheet (and will require the use of a current asset or will be replaced with another current liability).

Current liabilities include loans payable that will be due within one year of the balance sheet date, the current portion of long-term debt, accounts payable, income taxes payable and liabilities for accrued expenses.

Noncurrent liabilities

These are also referred to as long-term liabilities. In other words, these obligations will not be due within one year of the balance sheet date. Examples include portions of automobile loans, portions of mortgage loans, bonds payable, and deferred income taxes.

Stockholders' equity

This section of the balance sheet consists of the following major sections:

- Paid-in capital (the amounts paid by investors when the original shares of a corporation were issued)

- Retained earnings (the earnings of the corporation since it began minus the amounts that were distributed in the form of dividends to the stockholders)

- Treasury stock (a subtraction that represents the amount paid to repurchase the corporation's own stock)

No comments:

Post a Comment